賴柏錚

- 國立臺北大學會計學系博士研究

- 國立中興大學法律學系碩士

- 文字工作者

三、各類準則編碼原則

審計準則委員會制訂之會計師服務案件準則分類與編號規定,自民國111年12月15日起實施。

(一)審計準則委員會所發布各類準則依據

1、審計準則委員會所發布各類準則主要係參考國際審計暨確信準則理事會(IAASB)所發布準則(下稱國際準則)而訂定,並採用相同之編號,包含準則系列簡稱及編號。

2、所發布準則如非主要參考國際準則訂定時,將於該等準則之序號後加註「A」,以示區別。

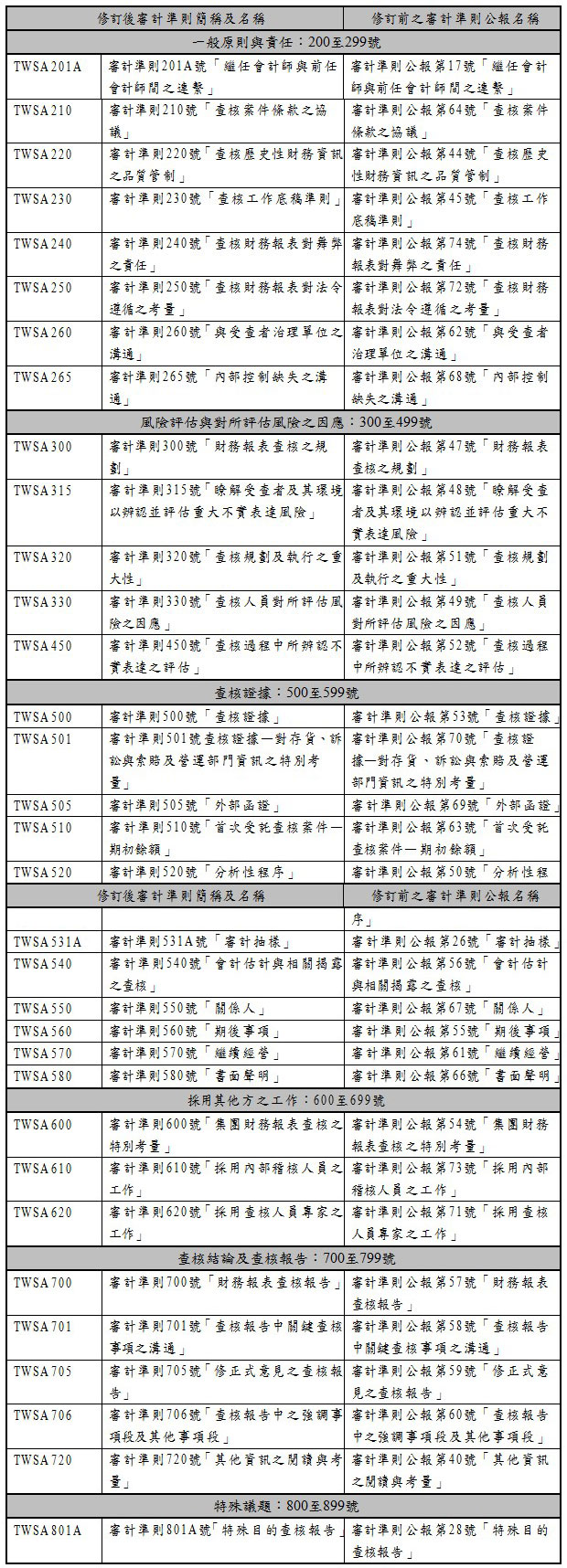

(二)「審計準則」之編號及規範之主題分述如下:

1、一般原則與責任:200至299號。

2、風險評估與對所評估風險之因應:300至499號。

3、查核證據:500至599號。

4、採用其他方之工作:600至699號。

5、查核結論及查核報告:700至799號。

6、特殊議題:800至899號。

(三)其他準則之編號

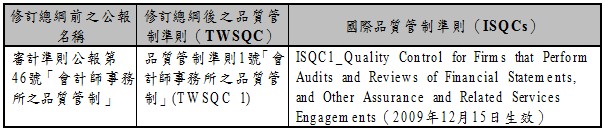

1、「品質管制準則」之編號係1至99號。

2、「核閱準則」係2000至2699號。

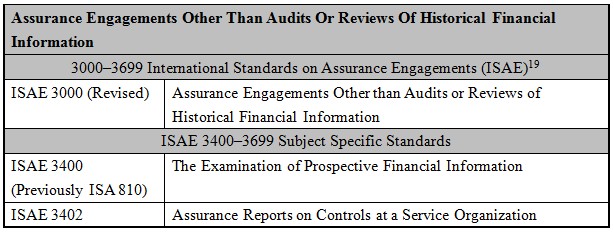

3、「確信準則」係3000至3699號。

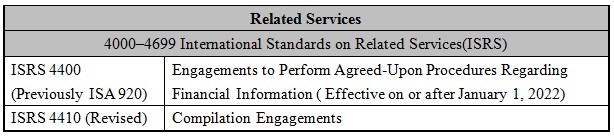

4、「其他相關服務準則」係4000至4699號。

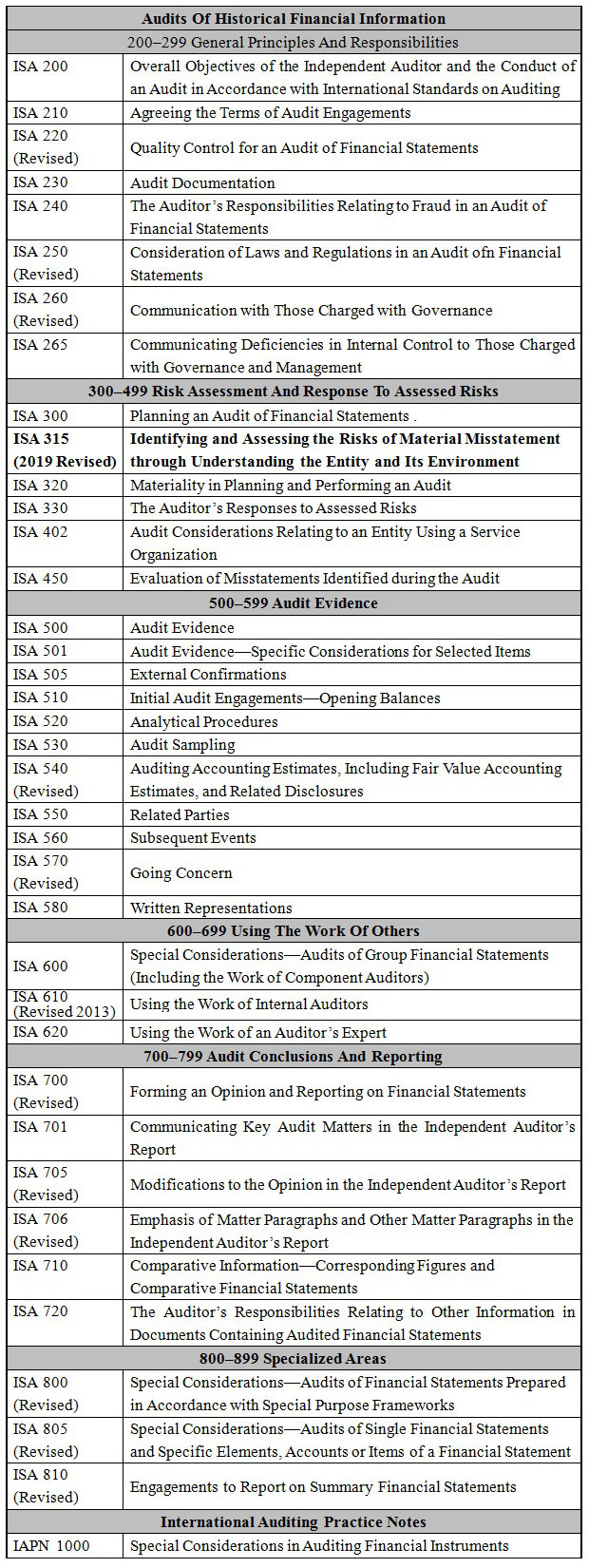

四、我國與IAASB「審計準則」架構

(一)我國「審計準則」架構

(二)IAASB「審計準則」(ISA)架構

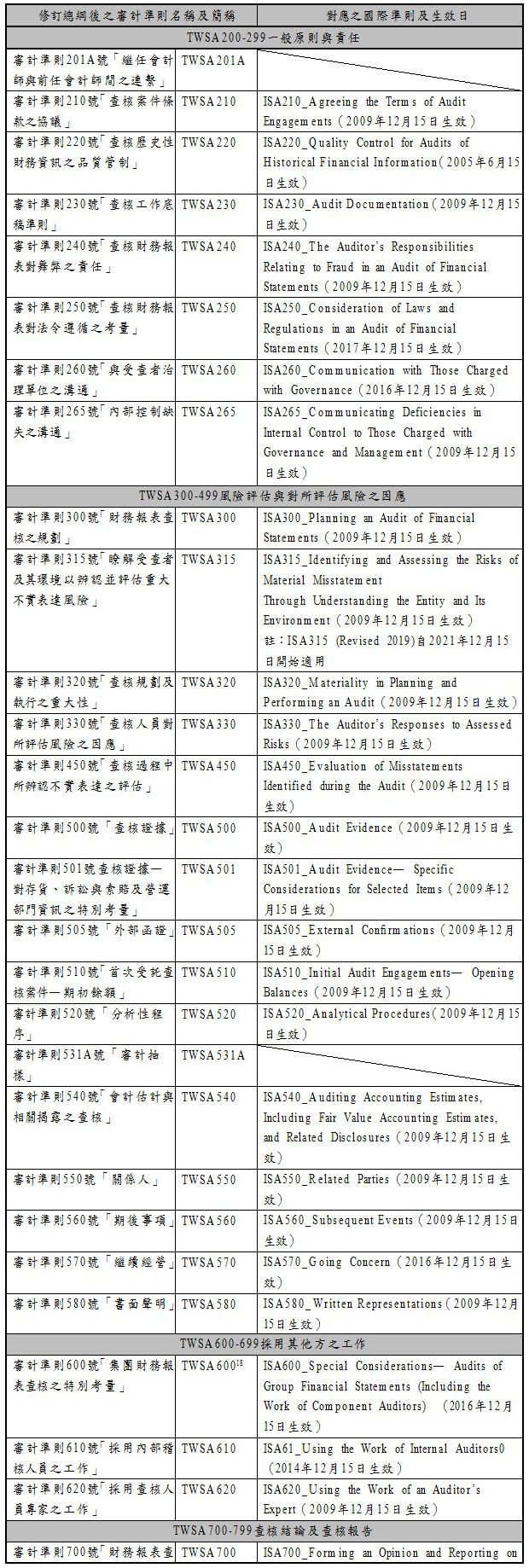

(三)修訂會計師服務案件總綱後我國審計準則與國際準則(ISA)對應關係

五、我國與IAASB「品質管制準則」

(一)修訂會計師服務案件總綱前後我國品質管制準則與對應之國際品質管制準則

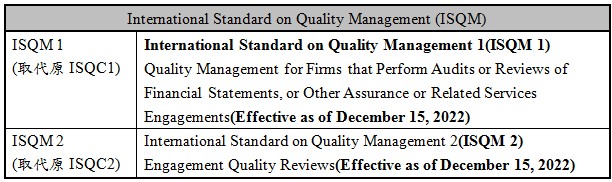

(二) IAASB「國際品質管制準則」(ISQM)制定現況

六、我國與IAASB「核閱準則」

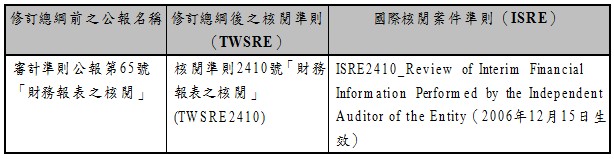

(一)修訂總綱前後我國核閱準則與國際核閱準則對應關係

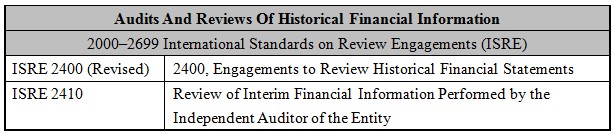

(二)IAASB「國際核閱案件準則」(ISRE)制定現況

七、我國與IAASB「確信準則」

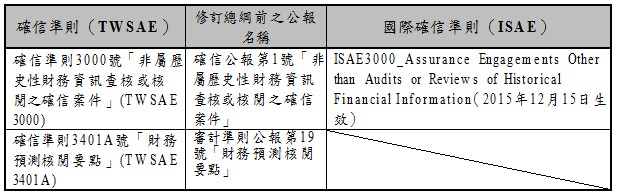

(一)修訂總綱前後我國確信準則與對應之國際確信準則

(二)IAASB「國際確信準則」(ISAE)制定現況

八、我國與IAASB「其他相關服務準則」

(一)修訂總綱前後我國其他相關服務準則與國際相關服務準則對應關係

(二)IAASB「國際其他相關服務準則」(ISRS)制定現況

資料來源

- 本文章有關會計師服務案件準則總綱著作權專屬於財團法人會計研究發展基金會所有,本人基於研究目的自財團法人中華民國會計研究發展基金會網站公報內容閱覽專區取得並摘錄援引。